Critical illness insurance calculator

Find out how a serious illness could affect your finances.

A serious illness can cost you a lot more than what your government health plan will pay for, once you factor in things like lost income, health-care expenses and other costs.

Take 2 minutes to get your results.

Financial impact of a serious illness for 1 year:

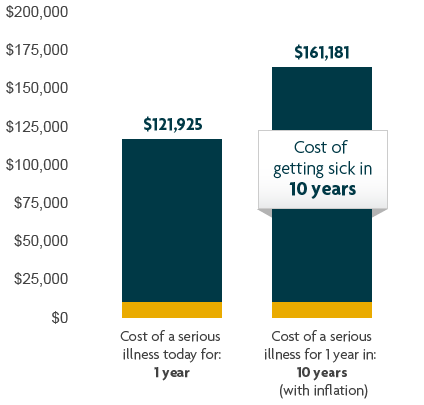

$121,925

Financial impact of a serious illness for 1 year:

$121,925

Explore the financial impact of an illness:

Find out how the impact of a serious illness on your finances can change by adjusting the numbers below.

Assumptions

Close- This tool assumes your salary will raise 3% per year.

- This tool assumes 2% average inflation.

- This tool assumes 4% average inflation for health-care costs.

- The tool assumes a default value of $25,000 for health-care expenses, and $10,000 for other illness-related expenses in case of critical illness.

- The results you received from this calculator is for your information only. The figures are not guaranteed, as they are based on assumptions that are certain to change.

Desired replacement income

CloseThis is the amount you’d need to cover day-to-day expenses during your recovery, such as utility bills and groceries. Remember to take into account any disability benefits you may receive.

Do not include other monthly expenses such as mortgage payments, property taxes, savings contributions and other debt payments.

Insuring your future health: Why inflation matters

CloseIt’s very important to factor in the effects of inflation when you’re thinking about how much critical illness insurance you may need. That’s especially true since the cost of health care is increasing faster than the overall cost of living.*

Speak to an advisor to help you plan for the protection you need now and in the future.

*Source: AON Canada Global Medical Report 2018Length of recovery

CloseThis is how long it might take before you can return to work full time. This will depend on the illness you’ve been diagnosed with, your age and your preferences for returning to work.

Illnesses such as Parkinson’s disease and multiple sclerosis will likely affect your ability to work for the rest of your life. And while you may recover from other serious illnesses, such as a heart attack, you may not be able to return to work full time.

Spousal income replacement

CloseThis is the lump sum amount of income your spouse or partner would lose if they want or need to take time off work to care for you as you recover from a serious illness. For example, if your spouse/partner took a month off to care for you, then this would be the amount of lost income for 1 month.

Health-care expenses

CloseThese are expenses not covered by your provincial health insurance or employer health benefits. They will vary according to the illness you are diagnosed with. Depending on your provincial and employer plans, health-care expenses could include items such as drug costs, private or semi-private hospital rooms, rehabilitation costs, deductibles, ambulance fees, in-home care and costs above coverage limits.

Other illness-related expenses

CloseThis could include travel for out-of-town treatment, home renovations for wheelchair accessibility and equipment such as hospital beds, as well as expenses for child care and housekeeping while you’re recovering. It could also include any income your spouse might lose by taking off time to look after you.

Monthly disability insurance payments

CloseThis includes the estimated monthly payment you would receive from your disability insurance coverage were you to become seriously ill and unable to work. This is usually a percentage of your current before tax income.

Leave this amount at zero if you do not have disability insurance coverage.

Get a free critical illness insurance quote

CloseSun Life offers two types of critical illness insurance products to meet your needs. You can buy Express Critical Illness Insurance online and Sun Critical Illness Insurance only with help from an advisor.

Be sure to compare critical illness insurance products so that you understand all of your options. If you’re not sure or have questions, speak with an advisor.

Compare critical illness insurance products